Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 2.3% for the week.

- Market expectations for several Federal Reserve interest rate cuts this year are dwindling, yet public equity market valuations have not yet suffered the wrath of a (slightly) more patient Fed.

In 2022, when the Federal Reserve raised interest rates at the fastest pace in its history, virtually all financial asset prices suffered, including stocks. Beyond the day-to-day noise, a company’s stock price can be thought of as the present value of the firm’s future cash flows (i.e., profits) per share. As interest rates rise, the present value of those future cash flows falls. This relationship has led many investors to claim that the Fed “controls” the stock market, to an extent.

Stock prices may fall when rates rise, but it is not simply “the math” as it is for bonds. The future cash flows generated by firms are much more uncertain than the interest and principal paid on bonds. Also, corporate profits occur into the distant future. Stocks do not “mature”. So, it is more accurate to say that when interest rates rise, then stock prices will fall, all else equal.

Despite higher interest rates and general economic gloom heading into 2023, the economy muscled past the Fed’s rate hikes and accelerated into the end of last year. To boot, inflation slowed, and futures markets began to price in several Fed interest rate cuts for 2024. The stock market rallied last fall, with many pointing to anticipated rate cuts as the catalyst.

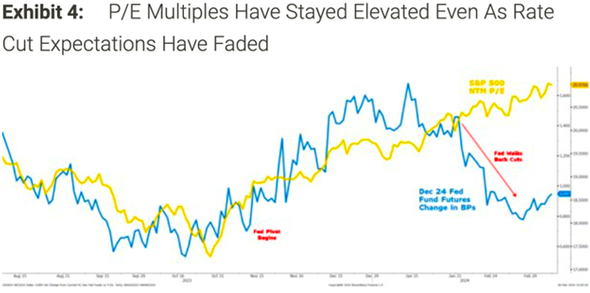

A chart from Morgan Stanley shows what appeared to be a close positive relationship at the time between expectations for generous Fed rate cuts last fall (the rising blue line) and the S&P 500’s price-to-earnings (P/E) ratio (the rising yellow line):

Sources: Sam Ro, Bloomberg, Morgan Stanley Research, March 2024

The disinflationary trend has hit a few road bumps in 2024. January and February inflation data was a touch warmer than markets had predicted. The Fed has been talking down the number of rate cuts as a result, and now only three Fed interest rate cuts are anticipated for 2024. This is why the blue line quickly dropped on the chart in January as highlighted by the red arrow.

The stock market, however, has continued its upward march. Although most investors consider higher rates to be bearish for stocks, equity valuations have not been compressed by new higher-for-longer interest rate expectations. Instead, the market’s P/E (the yellow line) has risen. The close positive relationship between expectations for rate cuts and equity market valuations has been severed for the last two months.

Perhaps the chart is showing that the recovery in the stock market since October hasn’t been about interest rates or the hopes for a more dovish Fed in 2024, after all. Maybe the rally has been driven by economic and corporate profit growth, which have proven to be far more resilient in the face of higher interest rates than anyone dared hope back in 2022.

Editor’s note: Our weekly update will be on hiatus until mid-April.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication.

Copyright Indiana Trust Wealth Management 2024.