Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 0.2% this week.

- Will US large-cap stocks continue their incredible outperformance of virtually every other asset class in the coming years?

The US stock market, gauged by the S&P 500 index, last reached its all-time-high in 2021. The following calendar year 2022 was one of the worst years on record for balanced portfolios of stocks and bonds, as the Federal Reserve cranked its overnight target interest rate up to douse inflation.

Weren’t the Fed’s actions and market’s reaction predictable? A few analysts did have a dour outlook for 2022, however at the start of that year it was not at all clear what path inflation would take or what the Fed would do. What if inflation proved to be transitory in a much quicker manner? What if the Fed decided not to pursue higher interest rates at the potential expense of employment?

In hindsight, events appear so obvious, but the future is almost impossible to predict – which is why diversification is so important. By definition, a diversified investment approach means that some strategies will underperform others, sometimes for uncomfortably long periods. In a sense, those underperforming strategies are the “cost” of an unknowable future.

The patience required for diversification is sometimes difficult to bear. The foremost current example of investor and asset manager patience wearing thin is for allocations to international stocks. The scrutiny upon allocations to developed and emerging markets equities is warranted: US stock market performance has crushed markets outside the US, in the aggregate.

The pertinent question when considering asset allocation decisions is, given current information, what is the probability that US stocks will continue such a wide outperformance?

Some of the outperformance of the US market has been driven by earnings growth. Fast-growing tech firms have been the source of outsized returns in the US market, whereas technology has a far lower sector weight in foreign markets. Macroeconomic conditions in the US have also been a boon for US corporate profits.

However, much of the disparity in returns between US and international equities has been driven by widening relative valuations. US stocks have simply become much more expensive than foreign stocks. Foreign stocks, by some metrics, have never been so cheap on a relative basis.

For the magnitude of US stock market outperformance over the last several years to continue, US equities would need to continue to grow more and more expensive. While that is possible, it is not likely. Valuations may not matter - up to the point that they matter a great deal.

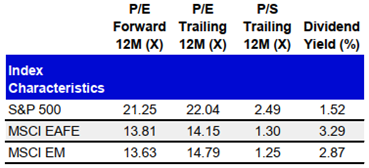

A chart from Invesco this week summarizes the current valuation disparity between the S&P 500 and developed foreign markets (MSCI EAFE) and emerging markets (MSCI EM). The US market is trading at a 55% premium on a P/E basis to foreign markets.

Source: Invesco, December 4, 2023

US mega-cap tech stocks have been the place to be for some time. Those firms have shown the ability to extract profits in a meaningful, recurring way. The recent focus on AI has been yet another tailwind for those names. It is hard to say, though, who the long-term winners will be from AI, or if other unpredictable shifts (such as those geopolitical in nature) will impact big tech firms in the coming years. Diversification will help mitigate the risks from an unknowable future.

Our weekly note will be on break until 2024. Everyone in the Indiana Trust Wealth Management family wishes our clients, our professional counterparts, and community partners a safe and happy holiday season!

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication.

Copyright Indiana Trust Wealth Management 2023.