Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, gained 1% for the week ending August 25.

- The Fed’s annual economic symposium is underway in Jackson Hole, Wyoming. Could the Fed be entering a ‘higher-for-longer phase” in its monetary policy cycle?

The Federal Reserve of Kansas City hosted its annual economic symposium this week in Jackson Hole, Wyoming. Why not hold the meeting in Wichita or Lawrence? The rumor is that legendary Fed Chairman Paul Volcker loved fly fishing in Wyoming, so by hosting the event there it assured his attendance in 1982. The meeting has become the buzziest gathering of economists and journalists on the calendar, with the central focus on the speech from the Fed chair, currently Jerome Powell, who spoke on Friday.

The meeting and speeches will veer into extreme wonkiness and heavy jargon, but the question on the minds of Mr. Powell and his brethren come down to this: why haven’t the Fed’s interest rate hikes – with a current target range of 5.25% to 5.5% - slowed down the economy and brought inflation down more quickly?

On the contrary, the latest projection for the third quarter from the Atlanta Fed’s GDPNow – a running estimate of GDP growth based on available economic data – is 5.9% real growth. Even should that number come down, which it most likely will, third-quarter growth will be far beyond what the Fed and most economists forecasted. What should the Fed do now?

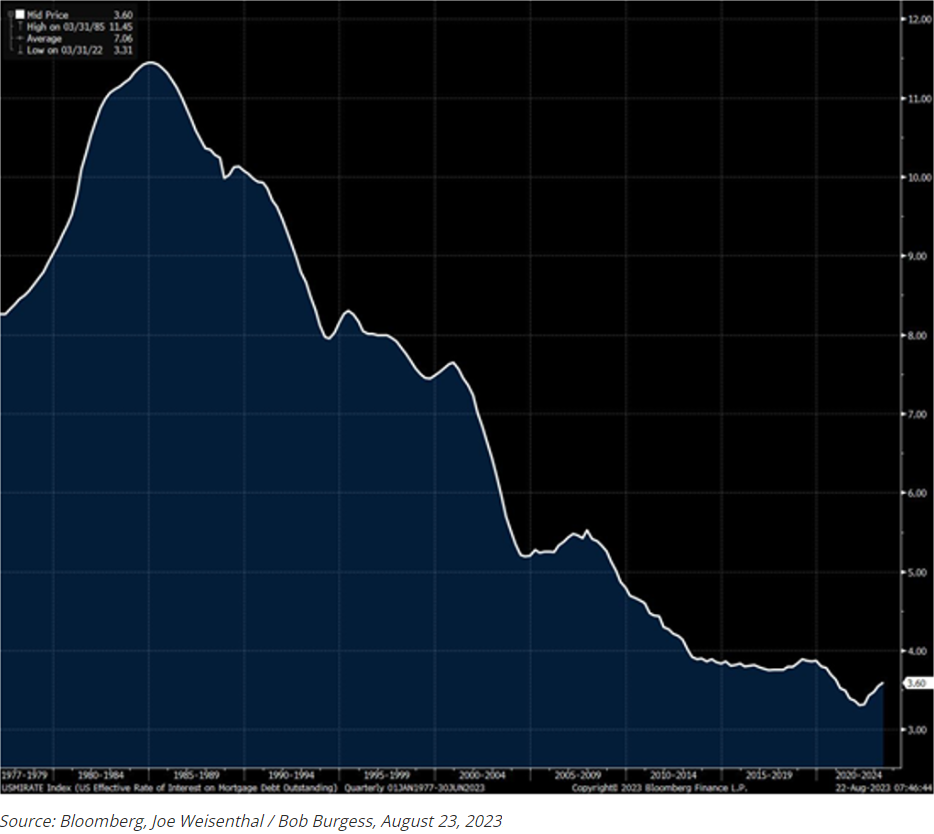

Mr. Powell may be wondering whether higher interest rates have been responsible for quelling inflation at all. For example, despite actual mortgage rates at 20-year highs, most Americans’ mortgage rates have barely budged. Almost all existing US mortgages are fixed-rate. The below chart of the average rate of interest on US mortgage debt over time, which currently stands at 3.6%, tells that story:

Joe Weisenthal at Bloomberg noted on Wednesday that in countries such as Australia and the UK, where mortgage rates are floating-rate, consumer spending has slowed much faster. Some of those central banks are now discussing interest rate cuts.

The transmission from higher interest rates to cooler household spending appears to take longer in the US than in other countries. In the meantime, the US economic expansion continues. Wages are growing faster than inflation. The US government’s fiscal budget deficit has widened. Capital investment is starting to accelerate.

Yet inflation is clearly falling. So, rather than hiking rates again, Mr. Powell and his colleagues may prefer instead to prolong the current “restrictive” interest rate target and wait it out.

This is partly why interest rates have risen in August and mortgage rates are at 20-year highs. A “higher for longer” Fed target interest rate outcome would carry implications for financial asset prices, some positive (short-term bonds), some negative (long-term bonds), and some which are harder to predict (stocks).

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.