Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, slipped 0.3% for the week ending August 11.

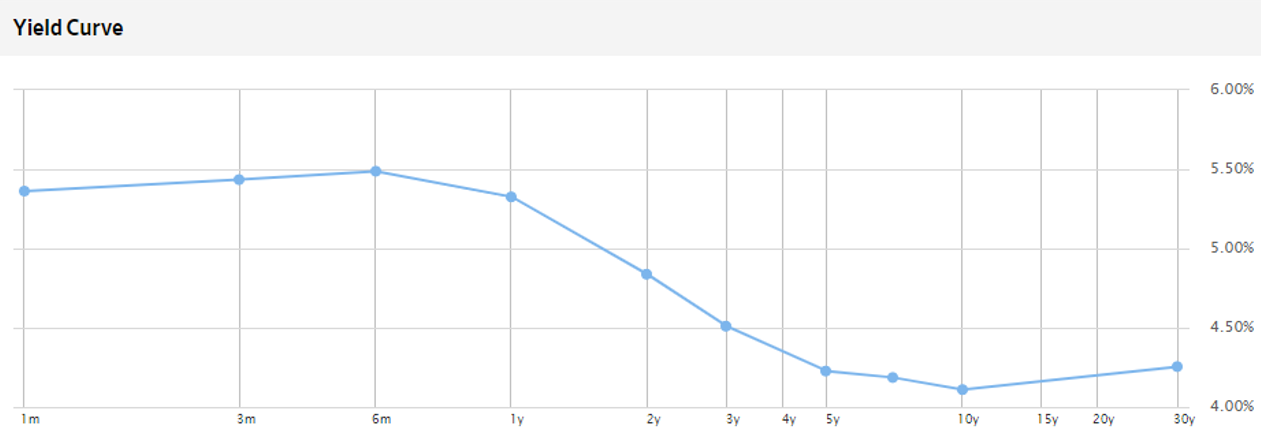

- The US Treasury market’s inverted yield curve is typically interpreted as a negative leading indicator for the economy. This week, a prominent Federal Reserve official made the case for a more benign interpretation of the situation.

The Federal Reserve raised its overnight target interest rate from zero to over 5.25% over the last 18 months. As the Fed essentially controls short-term interest rates, rates on short-term US Treasury bonds have shot higher.

Long-term interest rates have also increased, but not by nearly as much. This has created an inverted US Treasury bond yield curve. The curve has been inverted for some time: the two-year Treasury note has been above the ten-year since July 5, 2022. The yield curve currently looks like this:

Source: Wall Street Journal, August 11, 2023

Source: Wall Street Journal, August 11, 2023

One way of thinking about long-term bonds is that they may be decomposed into a series of short-term bonds, linked together through time. Thus, investors interpret an inverted yield curve as the bond market signaling that the Fed will be cutting interest rates in the future.

There may be other forces impacting the yield curve. The demand for long-term bonds may outstrip supply, for example. Pension funds and insurers need long-term bonds to offset their long-term liabilities.

Generally, however, the inverted yield curve’s message of future Fed interest rate cuts is viewed negatively by markets, because it is assumed that the Fed will be cutting interest rates in response to an economic slowdown or a recession. Inverted yield curves have preceded almost all recessions in the post-World War II era, although the timing from inversion to recession has varied widely.

In an interview this week, the New York Fed President, John Williams, described another, more benign reason that the Fed may need to cut interest rates in the coming years. He pointed out that real interest rates (“nominal” interest rates minus inflation) are currently rising without any action from the Federal Reserve because inflation is falling. Fed officials pay close attention to real interest rates as economists view real rates as driving investment and spending in the economy. Higher real rates curtail such activity, in theory.

Should the current disinflationary path continue, Mr. Williams notes that "if we (the Fed) don’t cut interest rates at some point next year (2024) then real interest rates will go up, and up, and up." By doing nothing, the Fed would be passively tightening monetary policy.

A scenario where the disinflationary trend continues, employment stays strong, a recession is avoided… and the Fed reduces its target nominal interest rate so that real interest rates stop rising would be bullish for economic activity and, likely, risky assets such as stocks.

Of course, the inverted yield curve could be the bond market signaling that it expects the Fed will end up breaking something and causing a recession with its recent interest rate hikes. However, the inverted yield curve could also reflect the bond market’s belief that the Fed will need to cut rates with or without a recession to keep real interest rates from rising too far.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.