Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, rose 0.7% for the week ending July 21.

- US investors who exclude foreign stocks from equity allocations are making an active choice to be less diversified relative to the global stock market. This may prove to be unwise in the long-term.

International equity diversification has not worked for US investors for 30 years. US asset managers are beginning to abandon foreign stock allocations, or, at least, reduce those allocations to insignificant “window dressing” levels. That way, portfolio managers can claim they still adhere to the key principle of diversification, one of the most fundamental ideas in modern finance.

Some investors argue that the US is simply the best place to invest and for companies to grow. This “US exceptionalism” case sounds good and there is some limited evidence to support it. It also justifies a home country bias for US investors.

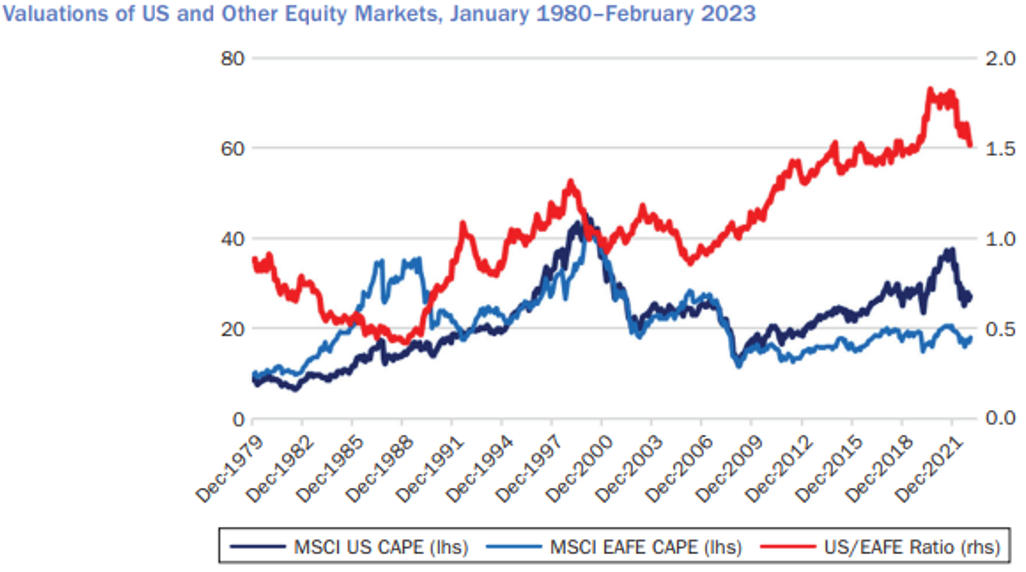

Earnings growth has been better in the US. However, a recent paper from AQR Capital Management notes that valuation changes explain almost all the US’s triumph over international stocks over the last thirty years. In 1990, US equity valuations were about half that of the MSCI EAFE Index of foreign developed market stocks (that fact alone is hard to imagine today). By the end of 2022, US stocks were 1.5 times more expensive – a tripling of relative valuations.

Some of the repricing of US stocks versus international was justified by earnings growth, but most of the outperformance was driven by the US market simply becoming more expensive. As the chart below shows, that trend – depicted by the red line – really took off after 2009.

Source: Cliff Asness, Antti Ilmanen, and Dan Villalon, AQR Capital Management. “International Diversification—Still Not Crazy after All These Years”, Journal of Portfolio Management, May 3, 2023

Source: Cliff Asness, Antti Ilmanen, and Dan Villalon, AQR Capital Management. “International Diversification—Still Not Crazy after All These Years”, Journal of Portfolio Management, May 3, 2023

The global equity market is relentlessly forward-looking. Those claiming that the US will outperform by a similar margin in the coming decades must be also claiming that US valuations will triple again relative to foreign stocks. Does a further and further widening of valuations make sense – even considering better US fundamentals such as earnings growth or US exceptionalism? Should investors extrapolate such dramatic US equity outperformance?

The arguments against foreign stocks also ignore that international equities outperformed the US for long stretches over the last fifty years. International equities beat the US for three of the past five decades – the 1970s, 1980s, and the 2000s.

International diversification is hard, but it is a good thing. It allows investors to partially mitigate the risk of any one country’s future underperformance, including the US. It is almost impossible to know when long-term cycles of US and foreign stock market leadership have turned. Relative valuations do not matter until they matter. The only way to execute diversification successfully is to have diversifying allocations in place ex ante rather than ex post those inflection points.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.