Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, rose 2.4% for the week ending July 14.

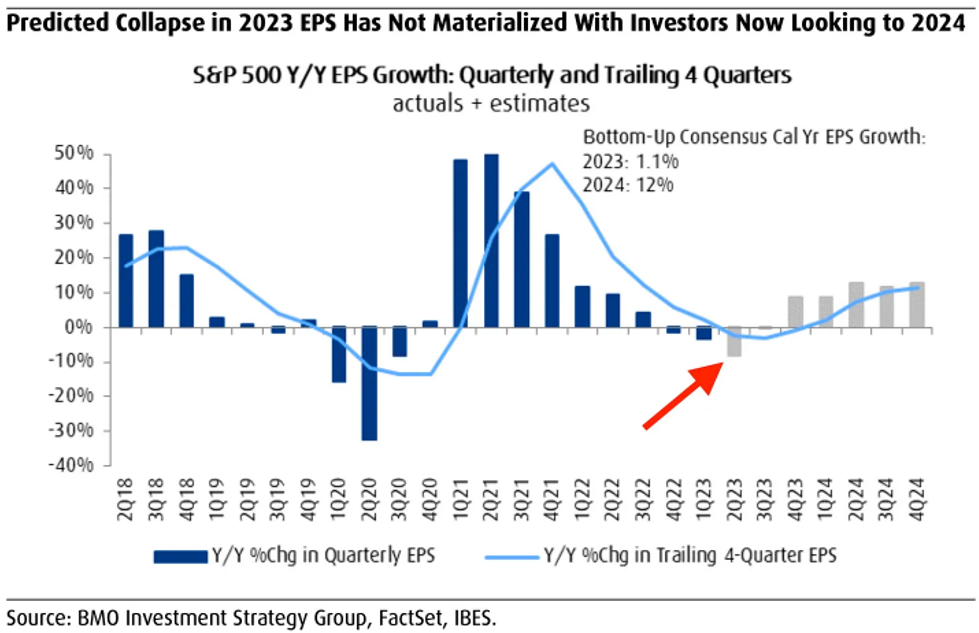

- This week, global equity and fixed income markets rallied, and the dollar swooned. Markets have digested the earnings situation in 2023 and are now focused on 2024 and beyond.

The Bureau of Labor Services released its monthly CPI report on Wednesday morning. Headline CPI rose by 0.2% in June. That result was cooler than expected. Year-over-year inflation in June 2022 was 9%. Through June of this year, it has fallen to 3%.

Since the start of 2022, the Federal Reserve has been raising interest rates and talking tough on its battle to bring inflation to heel. On more than one occasion, Fed Chair Jerome Powell opined that inflation would not trend to its 2% target without inevitable pain in the labor market because of higher interest rates.

That view is in the process of being disproven. Some combination of normalizing supply chains, time passing from general pandemic weirdness, and the Fed’s interest rate hikes have helped cool inflation - without the need to put millions of workers out of jobs, which some prominent economists predicted would be necessary.

The Fed is loath to declare “Mission Accomplished” at this point. Some at the Fed will argue that given the tight labor market and continued wage growth that inflation will not reach the Fed’s 2% objective, and that the current disinflationary path will be brief. Markets continue to price a 95% chance of a hike at the Fed’s July meeting.

Do equity markets or the economy still care about inflation or the Fed’s next 0.25% rate hike? Stock market investors are primarily concerned about profits. First quarter corporate earnings trounced lowly expectations, and the second quarter is off to a good start (based upon a very small sample size of the big banks and a few other firms).

BMO Capital’s Brian Belski recently wrote that even should earnings decline for the second quarter, investors fully understand that and are expecting double-digit earnings growth in 2024 and 2025. This helps explain why stocks have rallied so vigorously in 2023:

There are still a few economic tailwinds this year that could provide positive surprises for corporate earnings. The prime-age employment-population ratio just hit 80.9%, the highest figure since 2001. Household wages are still rising while inflation is slowing. This combination should continue to support household spending. Capital spending by companies is also rising, and that form of investment is an important source of corporate profits.

One Philadelphia Federal Reserve economist pointed to another boost for the US economy: the Taylor Swift Eras Tour. The Philly Fed reported that hotel bookings there rose the fastest since 2020 while Ms. Swift was in town. Chicago set a record for total hotel rooms occupied during her three-day stint at Soldier Field in June. The president of Visit Cincy, Julie Calvert, stated that "the economic impact Swift creates is staggering, as fans travel from far and wide to attend her concerts, filling hotels, restaurants, and local attractions. Swift’s influence on tourism is a testament to her ability to captivate audiences and drive economic growth."

Economists sticking to their recession calls for 2023 may need to shake it off.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.