Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, slipped 0.8% for the week ending May 6.

- The Fed raised its policy rate again this week by 0.25%, widely viewed as its peak rate. That may not mean rate cuts in 2023, however.

As expected, the Federal Reserve hiked its overnight target interest rate another 0.25% this week to a range of 5% to 5.25%. Mr. Powell stated the FOMC, the committee at the Fed responsible for interest rate decisions, would now take a data-dependent approach in its policymaking for the rest of 2023.

That is a much preferred approach to, say, a series of gut calls based upon general vibes. What data is the Fed emphasizing? This week, Mr. Powell repeatedly indicated that the Fed was watching labor market and household earnings data as evidence as to why the Fed may need to adjust monetary policy.

Employment is famously a “lagging” indicator. Economist Brian Romanchuk refers to the Fed’s approach as “reacting with a lag to lagging data.” It is natural to wonder how many more jobs can be created in an economy running at 3.4% unemployment. For those looking for storm clouds on the horizon, job openings and quit rates have fallen, and weekly jobless claims are inching higher.

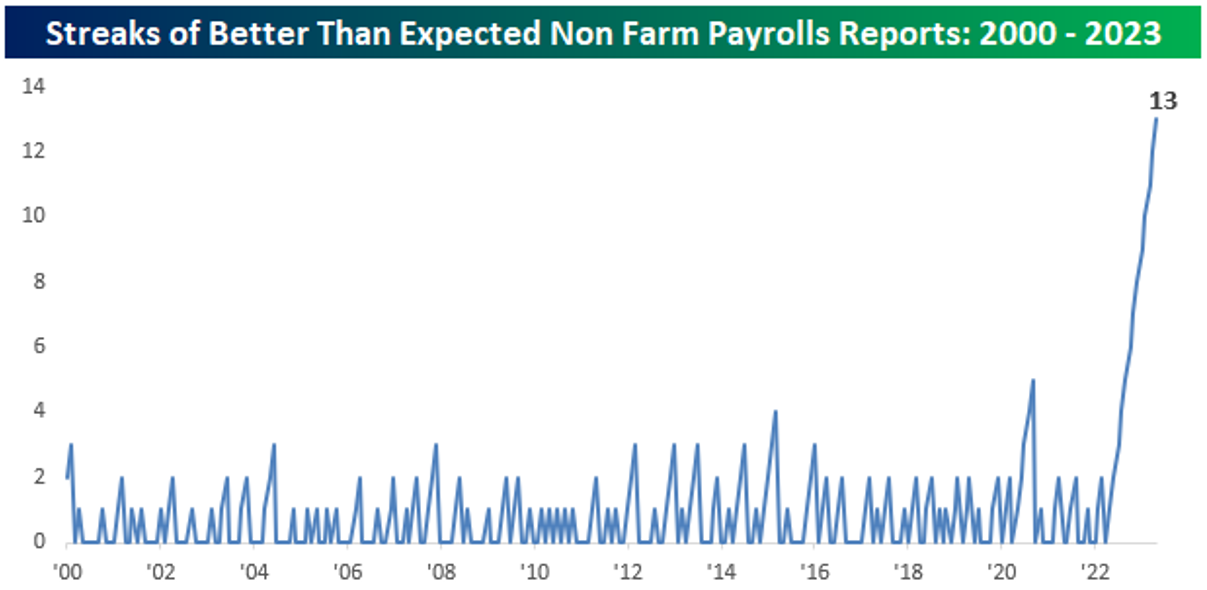

That said, the US economy continues to defy its naysayers and employment has not yet cracked. For economists, employment may be a lagging indicator… but it has been lagging for some time. The prime-age full-time employment rate just hit a 22-year high. The good non-farm payroll report from the BLS on Friday represented the 13th straight month of that report beating economist expectations, per the below chart from Bespoke Investment Group:

Chart: Bespoke Investment Group, May 5, 2023

As the Fed believes that employment must weaken for inflation to dissipate, it is no wonder it has not declared “Mission Accomplished”.

The macroeconomic environment feels like an endless game of point / counterpoint. The bond market is pricing in Fed interest rate cuts later this summer, yet a few prominent voices have opined that the Fed will be hiking rates further this year due to inflation’s persistence. Housing is normally seen as a leading indicator, and it has been strongly rebounding this year. Given turmoil in the banking sector, it seems logical that credit will begin to contract slowly over the coming months, which should put a crimp in housing. First quarter real GDP came in lower than expected, however much of that was due to inventory drag and final sales to domestic purchasers rose by its fastest rate since 2021.

As Mr. Romanchuk concludes, a plausible scenario is that the Fed’s policy rate moves sideways for a year or two, a rather boring outcome. The Fed could be forced to move faster based upon stress in the banking system, but the FOMC can probably wait a meeting or two to see what happens. Regional bank shares are under severe pressure, but a run on bank stocks is different than a run on a bank, and thus deserves a different policy response. Will the Fed raise rates further in 2023? Cut rates? Perhaps it will do nothing.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.