Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, fell 4.5% for the week ending March 11.

- One person’s spending is another person’s income. This means that excess household savings does not go away as households spend them down, and that spending may have long-lasting economic effects.

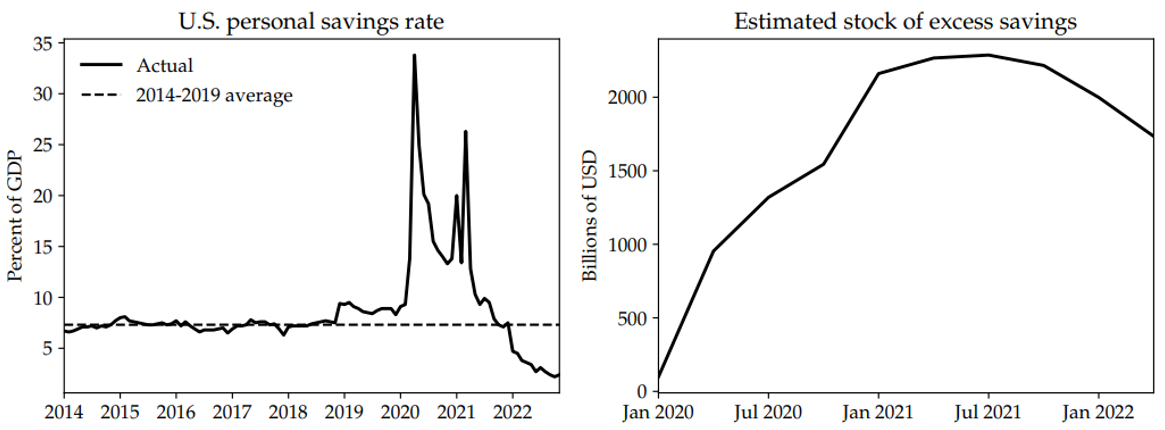

When the pandemic hit in 2020, the personal savings rate skyrocketed. Incomes fell, but spending fell much more. Under the circumstances, households could not spend even if they wanted to do so. The federal government also stepped in with the CARES Act, and subsequent fiscal measures, to directly bolster household income.

The combination of these events led to the creation of a large stock of “excess savings” by households. Economists have tried to estimate that stock of savings, and it was huge – at its peak, over $2 trillion.

Sources: BEA / FRED, FEDS Notes, 2022/2023

Households have been spending down their excess savings, which means their total spending has risen as a share of disposable income. This is evident in the chart on the left: the personal savings rate has fallen well below its multi-year average. Similarly, the estimated stock of excess savings has fallen.

It sounds logical that once the excess savings drains away from households – like water from a bathtub –that overall spending (or “demand”) will decline, and the savings rate will rise. Conventional economic wisdom is that, by now, most of the household excess savings has been spent and the effect upon the economy and the boost to corporate profits is over.

Gauging the duration of the impact of the household excess savings spenddown is a more complicated task than it appears because one person’s spending is another person’s income. Household savings do not drain like a bathtub.

The households that were able to save in 2020 and 2021 – households lower on the income scale – are also those who have a high marginal propensity to spend relative to income. Those households are spending.

The recipients of their spending will then spend some of that income. This spending will ricochet around the economy until it reaches households or businesses that have a lower propensity to spend relative to their incomes.

A recent paper from three economists[1] attempts to measure how long these effects might stick around. They estimate that it could take upwards of five years for the effects of the household spenddown of their excess savings to dissipate, even considering the Federal Reserve’s restrictive monetary policy stance (higher interest rates).

These models are only estimates, and there are crosscurrents to household spending that may appear. That said, if there is a persistent boost to aggregate spending from the spenddown of excess savings, it could help partially explain why the US economy has remained strong into 2023 and why cooling off inflation has been a challenge for the Fed. So far.

[1] “The Trickling Up of Excess Savings” by Auclert, Rognlie, Straub, February 2023

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.