Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, rose 1% for the week ending April 14.

- Investors continue to focus upon the US economy’s potential to slide into recession this year. Historically, the relentlessly forward-looking stock market has tended to recover before the economy.

In 2022, the Fed went on the fastest interest rate hiking cycle in the last forty years to squelch inflation, yet inflation stubbornly persists above the Fed’s 2% target.

Amongst other side effects, the Fed’s rate increases have caused heartburn in the banking system, although it is likely too early to say if higher rates will cause banks to significantly curtail lending. In a speech this week, new Chicago Fed President Austan Goolsbee noted that “at moments like this of financial stress, the right monetary approach calls for prudence and patience.” On Tuesday, Philadelphia Fed President Patrick Harker noted it can take 18 months for rate hikes to influence economic activity.

Not everyone at the Fed shares the “prudent and patient” approach. On Friday, Fed Governor Christopher Waller stated that “because financial conditions have not significantly tightened, the labor market continues to be strong and quite tight, and inflation is far above target, so monetary policy needs to be tightened further.”

What happened to the 18-month lag?

There appears to be growing debate at the Fed about future interest rate hikes. However, there is near consensus in the financial press and amongst economists that a US recession is unavoidable due to the Fed’s actions over the last year. The Fed itself believes that its rate hikes will cause an economic downturn.

A natural question for investors who agree with this assessment is, should risky assets such as stocks be divested in preparation for a recession?

While not perfect, the stock market is an efficient information processing system. It would be a stretch to believe that the possibility of a recession is “breaking news” for the market or that such an event could be profitably timed.

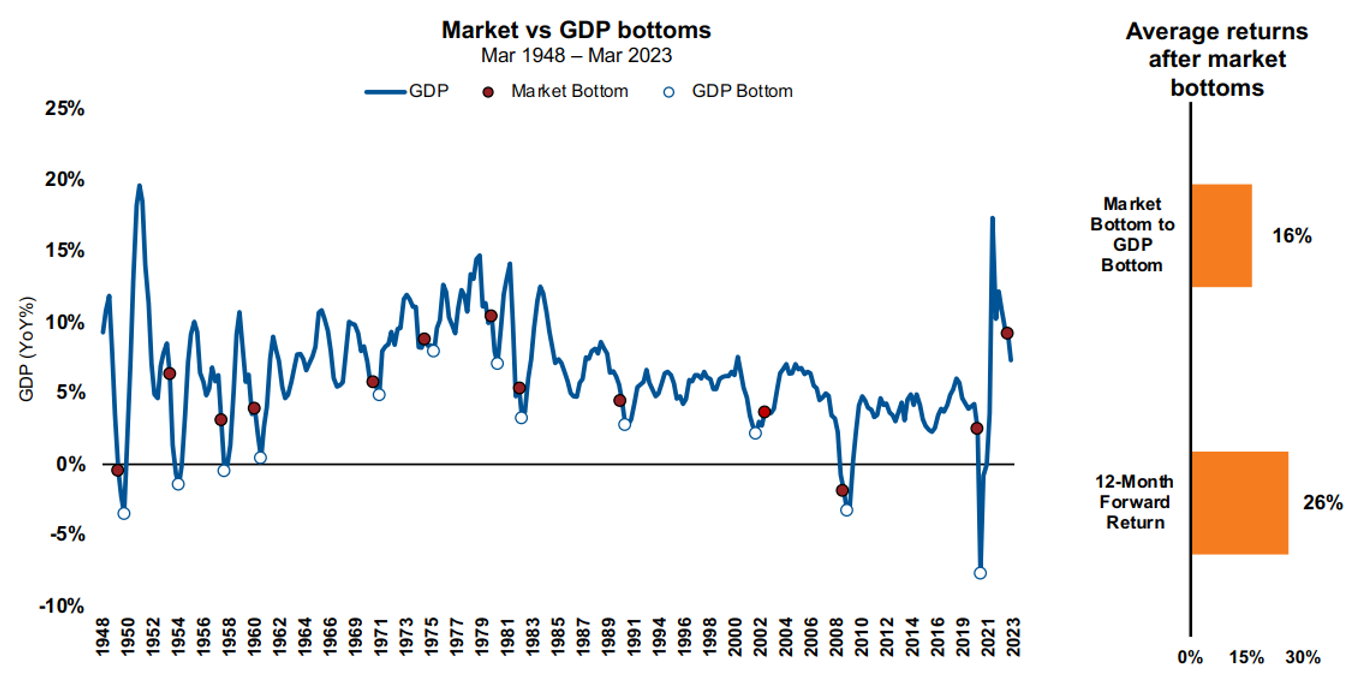

The stock market is also relentlessly forward-looking. Owning a share of a company’s stock means owning a share of that company’s profits from today into the distant future, decades from now. Because the market is constantly forward-looking, it tends to bottom and recover before the economy does during periods of economic decline.

A chart from Russell Investments nicely illustrates this tendency. The line chart is US Gross Domestic Product, or GDP, an effort to measure the growth of the economy. The market bottoms are the red circles on the GDP line, and the economy’s bottoms are the white circles.

Source: Russell Investments, March 2023

Market bottoms are only known in hindsight, as are GDP bottoms. Average returns after market bottoms to when the economy bottoms are 16%; 12-month forward returns from market bottoms are 26%. Historically, waiting in cash for the economy to recover is not a winning equity investment strategy.

______________