Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The US equity market, represented by the S&P 500 index, rose 1.5% for the week ending December 16.

- The jobs report delivered from the BLS on Friday hardly reflected an economy headed into a recession. Rather, it continued a trend of “Goldilocks” data supportive of a soft-landing for the U.S. economy.

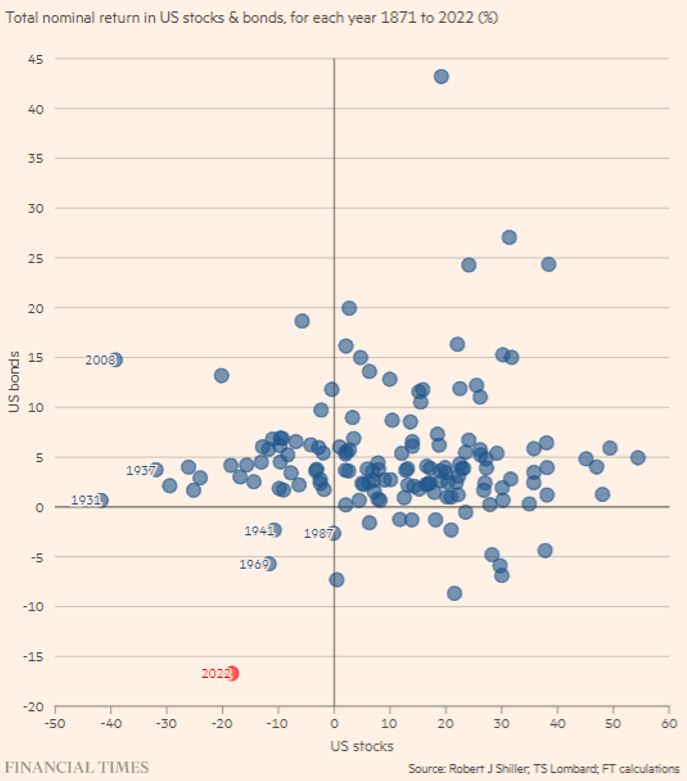

Happy new year to our clients, community partners, and professional colleagues! We begin the new year with a review of capital markets in 2022: virtually nothing worked. It was one of the worst years for stocks and bonds working in tandem since Ulysses S. Grant was President of the United States, per the chart below:

Source: Financial Times, January 2023

The main culprit behind financial asset pain last year was higher interest rates, engineered by the Federal Reserve to quell consumer price inflation. Tight financial conditions, including lower asset prices, is an express objective of the Fed in its quest to douse consumer price growth.

It is difficult to explain the channels through which higher interest rates lead to slowing inflation, but here the Fed and many economists are focusing upon wage growth. It is thought that high wage growth leads to high inflation. Economists fear the “wage-price spiral” model of inflation, although it is not obvious what drives a wage-price spiral. Is it the wages or the prices? Regardless, the Fed is trying to slow wage growth in the belief that it will slow services inflation and thus headline inflation, avoiding the spiral entirely.

Virtually every economist is predicting a recession in 2023 because they believe that wage growth will not moderate unless unemployment rises. Rising unemployment is not the desired Fed outcome, but if that is what it takes to slow wage growth and inflation, then, for the Fed, so be it.

Recessions matter for stock markets. Shrinking economies are not good for profit growth. A recession would be okay for bond markets in the short run because it would allow the Fed to pivot to interest rate cuts. Falling yields push up bond prices.

Although it would be hard to imagine given the Fed’s rhetoric, the financial press coverage, and prominent economists on social media, it is possible that a “Goldilocks” or “soft-landing” scenario plays out. How would such an outcome look? The U.S. would continue to create jobs, unemployment would remain low, wage growth would slow, inflation would drop, and there would be no recession.

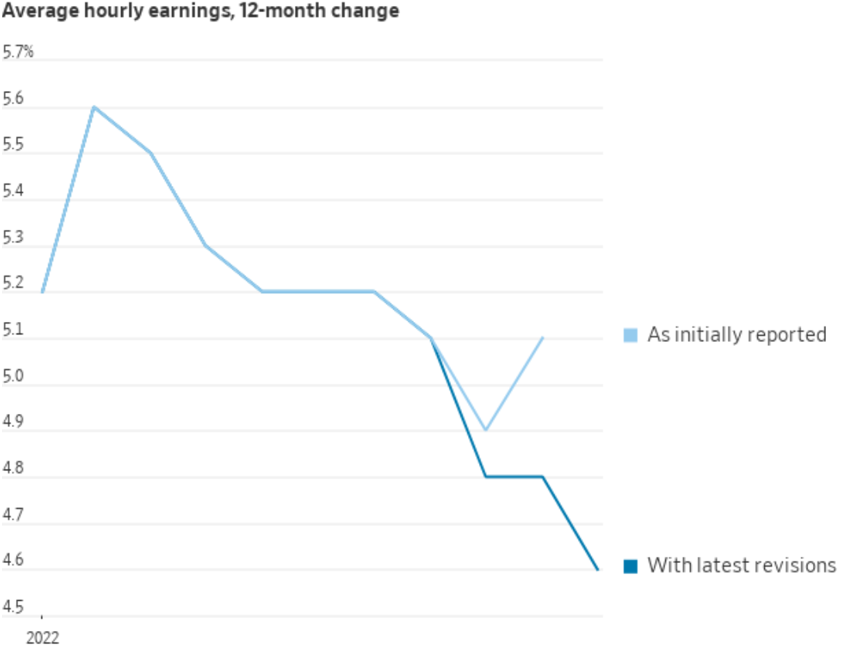

That scenario is what has been delivered in the data over the last three months. The Bureau of Labor Statistics (BLS) December jobs report released on Friday could have been written by Goldilocks herself: 223,000 jobs were created, and headline unemployment fell to 3.5%, the lowest since 1969. Perhaps most importantly, wage growth slowed – and November’s monthly wage growth number, which was at the time quite hot and of utmost concern to markets, was revised lower.

Source: Wall Street Journal, Labor Department, January 6. 2022

Given high inflation in 2022, the chart above doesn’t look much like a wage-price spiral.

One issue with the Goldilocks scenario is that professional economists do not like their models to be wrong. Even with slowing wage growth and falling inflation, many at the Fed will argue for continued strict monetary policy until pain is felt in employment. Should the soft-landing scenario continue to be supported in the data over the first half of 2023, the Fed will find it harder and harder to explain its tight financial conditions stance.

_______________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2023.