Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, fell 2.1% this week.

- Corporate fundamentals may help explain why the stock market has been composed, for the most part, in the face of events in the Middle East.

The S&P 500 is approaching “correction” territory, down almost 9% from its January all-time high. Drawdowns of this magnitude have been a regular occurrence in the market. Given events in the Middle East, the current pullback has been rather orderly.

Explanations abound for the US stock market’s composed response to the abrupt removal of 20% of the world’s oil supply. Stock market bears are describing it as complacency, a “deer-in-headlights” reaction. Perhaps most investors figure that a de-escalation and resumption of oil tanker transit are inevitable, a perfectly reasonable belief.

More salient reasons for the market’s stiff upper lip may be that corporate earnings per share (EPS) growth has been tremendous, and expectations for 2026 are through the roof. The S&P 500 has delivered five straight quarters of earnings growth for the first time in almost ten years. Fourth-quarter year-over-year EPS growth was over 14% with all eleven industry sectors in positive territory.

The market’s forward price-to-earnings (P/E) ratio, which takes the price of the stock market divided by expected earnings over the next year, peaked at 23.1x last October. That is a historically high valuation reading, only surpassed in 2020 (briefly) and during the dot-com era of the early 2000’s. The P/E now stands at 19.7x, a substantially more reasonable (yet still elevated) valuation.

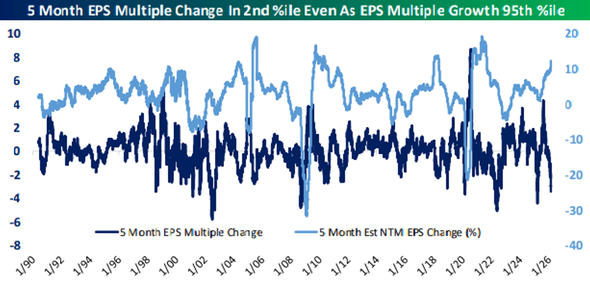

As George Pearkes from Bespoke Investment Group notes, the P/E ratio’s decline stems from changes in both the numerator (as prices have mildly declined) and the denominator. Over the last five months, equity analysts have increased earnings growth expectations by 12.3% - a huge positive change in the outlook. That lofty change to expected EPS growth is 95th percentile historically, while P/E’s drop over the same period is 2nd percentile. This dynamic – estimated EPS up 12.3% coupled with a precipitous drop in the P/E – is a rare occurrence, not seen in recent market history.

Source: Bespoke Investment Group, March 26, 2026

Those expected earnings may or may not materialize. However, this episode is a reminder that corporate fundamentals – sales, margins, earnings – can improve valuations quickly. It may also explain why the market has remained relatively steady during the Hormuz saga, so far.

Editor’s note: our weekly update will be on hiatus until mid-April.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2026.