Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, fell 1.7% this week.

- The oil supply disruption in the Persian Gulf may lead to second-order effects, but the US economy is less oil-reliant than in the past and less exposed to large swings in oil prices.

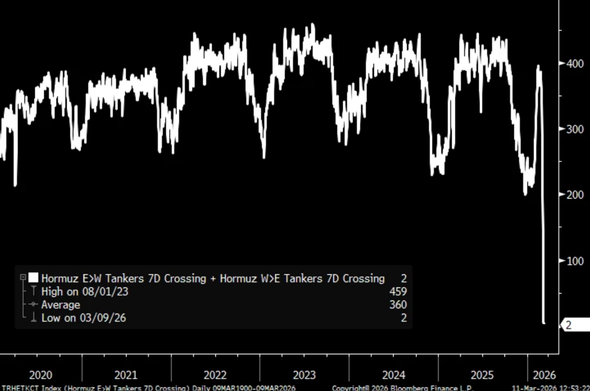

Global capital markets are hyper-fixated on the price of crude oil. Roughly 20% of the global oil supply traverses the Strait of Hormuz. As the chart below shows, about 360 oil tankers typically cross the Strait on a weekly basis. As of the seven days through Wednesday of this week, there were only two.

Source: Bloomberg, George Pearkes, March 11, 2026

Considering events in the Middle East, stock markets have been relatively calm. The S&P 500 is only off 3% this year. The muted response from short-term traders so far may be rational - in the face of so many unknowns, there may not be a good reason to do anything from a trading perspective. For long-term investors, geopolitical risk is nothing new.

The air pocket in the global oil supply that has been created over the last two weeks will create second-order effects. Some economists have been whispering about the potential for a return of “stagflation”, referencing the potential for an inflation boost from rising energy prices coupled with February’s modest upward tick in unemployment. Stagflation is a term that became ubiquitous in the 1970’s, during that era’s energy crisis.

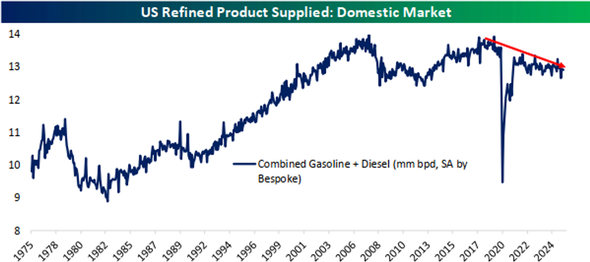

It is not the 1970’s anymore. The global economy – and the US in particular – is less dependent on oil than it was in the past. Hybrid and EV market penetration has led to a decline in US fuel consumption. Gasoline consumption is well off its peak in 2007, and barrels supplied per day stand roughly at the same level as 25 years ago. The US economy has grown by 70% over that time.

Source: Bespoke Investment Group, March 10, 2026

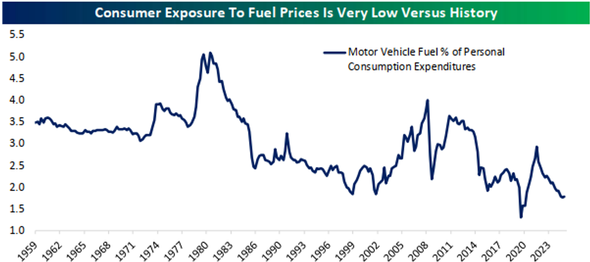

Also, the US consumer is less exposed to oil prices now than in the 1970’s and 1980’s, when almost 5% of consumer spending was on vehicle fuel. That figure now stands below 2%.

Source: Bespoke Investment Group, March 10, 2026

An oil price shock may have reverberating effects that will have an impact for some time, but it stands to reason that the US economy is somewhat less exposed to large swings in oil prices than in the past.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2026.