Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, slipped 1.4% this week.

- There has been much handwringing over the concentration of the US stock market in a few companies. The US is not the only stock market with this issue, and these fears are likely overblown.

South Korea’s stock market is on a tear. An ETF tracking the Korean market is up over 35% so far in 2026 and has gained 142% in dollar terms over the last twelve months.

These performance numbers require some context. Two companies make up 50% of that market: Samsung Electronics represents 30%, and SK hynix weighs in at 20%. Both companies are leaders in the memory semiconductor industry, which has become a major focus of the AI buildout.

The US stock market has also become concentrated in a handful of names in recent years, although not to the extreme of the Korean market. Only seven companies make up 33% of the S&P 500, a historically high concentration of market cap weight in so few names.

Is concentration a problem – are there too many eggs in too few baskets around the globe? A column from Jason Zwieg at the Wall Street Journal this week argues that it is unwise to attempt to avoid concentrations in market structure.

He notes that over the last 90 years, if an investor cut back on US stocks during periods of high concentration and added to stocks when concentration was declining, one would have earned about 1% less per year than a buy-and-hold strategy. The reason? Mr. Zwieg points out that, by definition, market concentration goes up whenever winning stocks keep winning. Market weights of individual stocks are not frozen in time.

The biggest stocks also have exposure to multiple economic sectors, typically. Microsoft runs hundreds of businesses, for example, so in a sense they are intrinsically diversified.

Allocations to foreign markets add another level of diversification by providing a different blend of economic and currency exposure versus the US. The top names in global markets can offer a different opportunity set – even where it appears there is significant economic sector overlap.

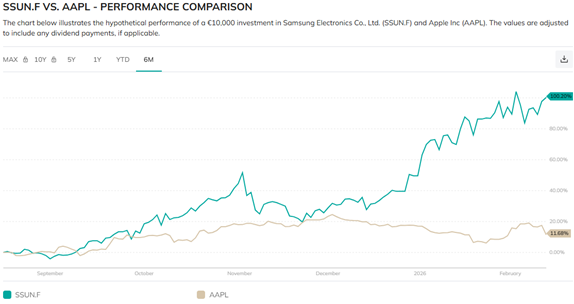

For example, Samsung competes directly with Apple (refer to the endless patent lawsuits between them). However, Samsung is vertically integrated where Apple focuses on design. Apple’s relatively capital-light approach has been favored by investors for years, yet it is Samsung’s capital-intensive memory chip manufacturing business that has propelled its stock up 100% over the last six months. Apple has gained 12% over that time. The best course of action is to own both.

Source: PerformanceLab, February 13, 2026

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2026.