Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, was flat for the week.

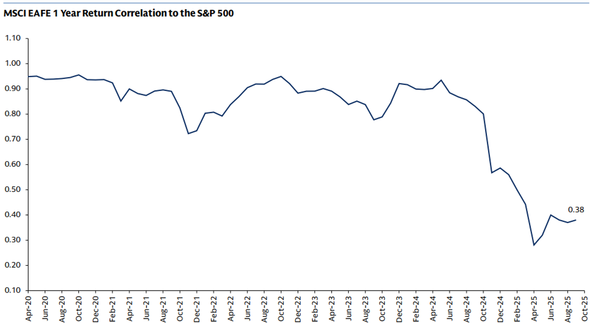

- The correlation of returns between foreign stock markets and the US market has declined significantly over the last year, a positive development for globally diversified portfolios.

Modern portfolio theory (“MPT”) was developed in 1952 by legendary economist Harry Markowitz. While the math surrounding the theory is a bit daunting, its core principle is easily understood: blending assets that do not move in the same direction under the same market conditions reduces portfolio volatility. Diversification smooths the ride.

Assets with a correlation of “1” move together in lockstep. Those with a correlation of “-1” move in completely opposite directions, and assets with a correlation of zero move completely randomly versus one another.

The widespread adoption of modern portfolio theory resulted in great focus upon correlations between asset classes. Thanks to Professor Markowitz, assets which have low correlations – less than “1”- were deemed very attractive for diversification purposes. International equities were noted for their low correlations to US stocks while retaining a similar expected return profile. US investors began snapping up foreign stocks for diversification purposes.

Like most market-based strategies, once a good idea is widely adopted, its original benefits can become diluted. Over the years, global financial markets became increasingly interconnected, in no small part due to the new diversification principles underpinning MPT. Foreign stock market correlations to the US market rose over time, and in recent years their correlation has been close to “1”.

There are plenty of reasons to make portfolio allocations to foreign stocks apart from their statistical properties. There are big, important companies listed in markets outside the US worthy of investment. Also, a dose of unhedged exposure to non-US dollar assets can be a portfolio benefit. Admittedly, however, the portfolio volatility-reducing case for foreign stocks lost its luster.

Correlations can change, and in recent years, correlations between the US market and developed foreign markets have declined. This is good news for investors adhering to the core principles of diversification espoused by MPT. One reason for the recent decline in correlation could be that the US market’s economic exposure has become more concentrated in the technology sector compared to foreign markets. The dollar’s recent weakness is also a reversal from recent years and could play a role.

Source: Goldman Sachs Asset Management, as of 9/30/25

Goldman Sachs calculates that the correlation between developed foreign markets (represented by the MSCI EAFE) and the S&P 500 has declined to a captivating 0.38 over the last year. Should correlations remain low, foreign stocks may once again become an important volatility dampener in US investor portfolios.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.