Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 0.7% for the week.

- After a brief pause at the start of the year, the US consumer has rebounded in 2025. It may be more than just the wealth effect from higher stock market prices that is explaining consumer strength.

The US consumer has rebounded after a brief pause earlier this year. Some have posited that the consumption “boom” in the second half of 2025 is “K-shaped”. That is, the top income and wealth deciles are doing quite well due to rising stock market prices, thus driving overall US household consumption (a “wealth effect”), whereas households in lower deciles are hardly spending any money at all and falling further behind.

In a note this week, the economist Mattew Klein wrote that there are alternative interpretations of the data. Wealthier Americans do play a large consumption role, but that is always the case. Their current contribution is not outsized compared to prior periods.

Also, while large price increases in the stock market can affect spending behavior, he notes, the market also reflects changes in behavior. Much focus has been put on AI-adjacent stocks driving the market, yet industrial and financial names have kept pace. Stocks exposed to discretionary consumer spending have crushed defensive names so far in 2025. In other words, investors have been betting that broad swaths of the US economy are doing well.

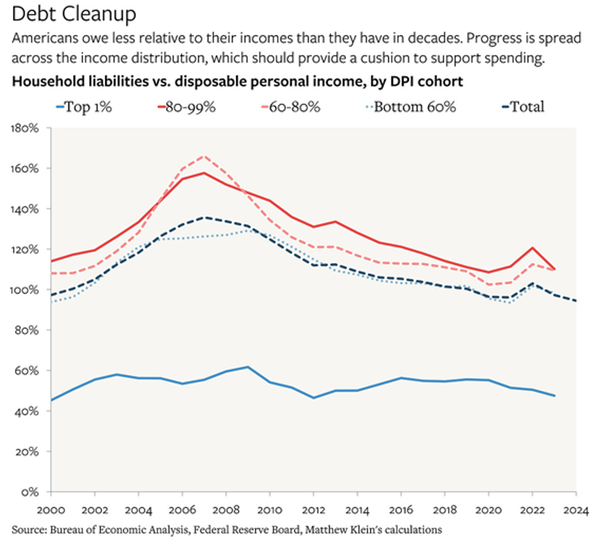

From a household balance sheet perspective, debt is down relative to assets across multiple metrics. In the aggregate, Americans hold more cash relative to debt than at any point in decades. While the top earners have seen the largest gains of cash relative to liabilities, the increase in cash has occurred across the income distribution.

Relative to income, it is much the same story. Americans owe less than they have in years, across the income distribution, per Mr. Klein’s chart below:

Household savings skyrocketed post-pandemic because of extraordinary US government fiscal support coupled with a lack of ways to actually spend money. In subsequent years, those savings have been spent, particularly by lower earners with a higher propensity to spend relative to income.

However, household savings do not drain from an economy like water from a bathtub. It ricochets around until it reaches households or businesses that have a lower propensity to spend relative to income. A research paper from 2023 modeled that the impact from the federal government response to the pandemic and subsequent household saving behavior may take more than five years to dissipate.[1] It could be this process is ongoing, explaining some of the broad-based strength of the US consumer.

[1] “The Trickling Up of Excess Savings” by Auclert, Rognlie, Straub, February 2023

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.