Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, slipped 2.4% for the week.

- There are some meaningful contrasts between US technology stocks today versus the tech sector 25 years ago.

The consensus across famous asset managers, economists, and the chairman of the Federal Reserve is that the US stock market is expensive. Measured by its price-to-earnings (P/E) ratio, the stock market appears pricey.

The US market has become expensive because it has been taken over by the technology sector. Relative to the overall market, US tech has never been so large. As the tech sector assumes a growing share of the market, the valuation of the overall market rises because tech stocks carry a valuation premium versus other sectors. That premium exists mainly because of expected earnings growth.

Rising tech stock prices (mainly due to AI hype) have led to comparisons between the environment today and that of the dot-com era around the year 2000. That era led to a dreadful stock market decline.

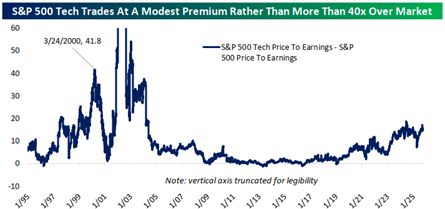

Is the US market approaching a dot-com-esque bust, à la 2000? While it is usually heresy to claim “this time is different”, there are some meaningful contrasts between tech stocks today versus the turn of the millennium. First, a chart from Bespoke Investment Group shows that in 2000, the tech sector traded at a 41.8x valuation premium over the rest of the market. That premium is only about 10x today.

Source: Bespoke Investment Group, October 3, 2025

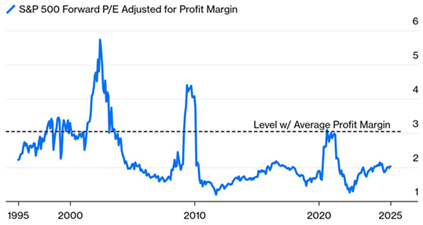

Ultimately, profits and earnings growth are what matter for stocks. Michael Wilson, equity strategist at Morgan Stanley, makes the point that the S&P 500 looks nothing like the stock market bubble in 2000 because profit margins are much higher now than the dot-com era. This is reflected in the next chart, showing the P/E of the market divided by its profit margin. Taking profit margins into account, valuations look cheap versus 25 years ago:

Source: Bloomberg, October 9, 2025

This chart also shows that should profits suffer and revert to their long-term average, then stocks would indeed look much more expensive. The bright side? There is not much evidence that profit margins are mean-reverting. Profits may continue to be strong, particularly for mega-cap tech firms. That is certainly what the market expects, for now.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.