Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, was up 1% for the week.

- The term “bubble” is freely floating in the financial and social media discourse. Do rising US stock market valuations point to bubble formation?

Across financial and social media, there is consensus that all the vast sums spent on AI and the resultant valuations of the big “hyperscaler” stocks are beginning to fit the classic definition of a “bubble”.

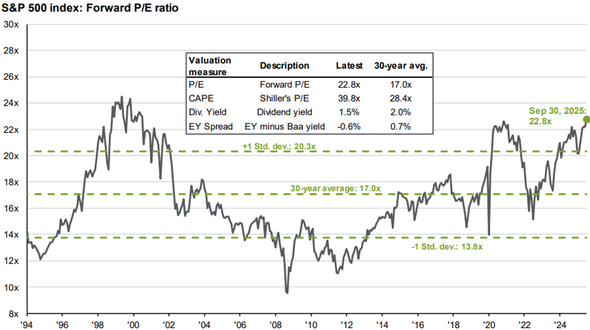

The US stock market, dominated by big tech names, looks expensive on a price-to-earnings (P/E) basis when compared to its 30-year history. The chart below from JP Morgan shows that relative to expected earnings over the next year, the stock market is as expensive as it has been since 2002. Relative to an inflation-adjusted trailing 10-year period of earnings, a valuation metric known as “CAPE”, stocks are 40% above their 30-year average.

Source: JP Morgan Asset Management, October 2025

It is hard to extrapolate a market-timing signal from this chart. P/E ratios are poor predictors of short-term performance. Stocks may continue to rise from here. Valuations do somewhat better at explaining long-term returns, but it’s not a mechanical relationship. Is thirty years the right timeframe to compare valuations? Should a market valuation metric use ten years of trailing earnings history for its current measurement? Perhaps not.

Corporate earnings drive stock prices over time, and earnings and revenues are expected to grow strongly next year for publicly traded companies, which is what the JP Morgan chart reflects. Most of the AI cash burn – which is well into the hundreds of billions – is occurring at private companies such as OpenAI and Anthropic, as the economist George Pearkes noted this week. In those private markets, capital raising continues apace, and valuations are stratospheric.

So far, investors haven’t demanded results in the form of revenue or free cash flows from AI companies. Eventually, all that spending will need to result in proportional revenues. There is no deadline that investors have placed upon that, however. So far, the opposite is true: the more money spent on AI, the bigger the valuation that is attached by investors.

No one knows how long the AI investment cycle may last, and investors are provided daily evidence that it is continuing. Mr. Pearkes notes that given the element of human nature, it is inevitable that an overshoot occurs. Evidence of peak AI sentiment and enthusiasm, however, has not yet taken place. It may be difficult to realize in the moment if or when it does.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.