Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, was flat for the week.

- Gold has soared in 2025, outperforming most domestic stock markets around the world. What is propelling gold prices upward?

Gold, that yellow metal with limited industrial purpose and which pays no dividends or cash flows to its investors, has skyrocketed in 2025. Through Wednesday, gold was up 42% for the year. It is on track for its best performance since 1979, a year when markets freaked out about inflation – amongst other geopolitical events – and sent prices for the commodity up by over 100%.

There is certainly no lack of available narratives to explain gold’s rise in 2025. A quick perusal of the news lays out the following possibilities:

- AI will generate tremendous economic uncertainty in the coming years. Gold is a “fear asset”, and its rise is a signal of investors trying to hedge a tumultuous future.

- Lack of faith in the “system” and political uncertainty are driving investors to the “safe haven” of gold.

- The dollar has weakened, and as bullion is priced in dollars, that has made gold more attractive to the rest of the world.

- The Federal Reserve’s independence is under political threat. Investors are betting on a crisis.

- The Federal Reserve will cut interest rates further, which will make gold more attractive as the opportunity cost will fall for holding a non-interest bearing lump of metal.

- Central banks around the world – particularly China – are diversifying their reserve assets away from the dollar and into gold.

These explanations sound tidy and will appeal to various investor biases. The multitude of narratives show the difficulty in attempting to place an intrinsic value on gold. It is slippery.

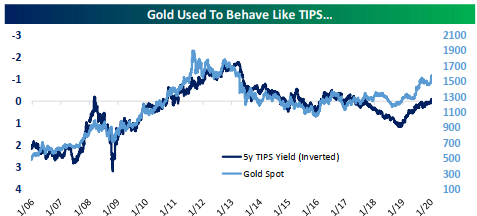

The last two bullet points deserve some attention. Until 2020, real interest rates (interest rates minus one’s preferred definition of inflation) had done a good job explaining gold’s returns. As real interest rates fell, gold rose, behaving a bit like an inflation-protected bond (known as TIPS).

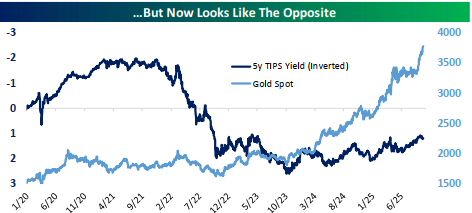

Since then, however, gold is acting like the opposite. When real interest rates plunged post-COVID, gold did nothing. And when the Fed cranked up interest rates in 2022, pushing real rates up, gold rallied strongly.

Not even the old reliable real interest rate indicator seems to work anymore. It must be that China is buying all the gold? Unfortunately, the evidence does not point to China as the culprit. Looking at months when China has bought gold, the correlation between those times and gold prices is negative, per Bespoke Investment Group.

The market for gold represents less than 1% of global capital markets. In that context, it is not very large. As such, gold has higher exposure to short-term trading momentum, market sentiment, and liquidity constraints than other financial markets. ETFs tied to gold have seen massive inflows this year. Last Friday witnessed the largest daily inflow into gold ETFs (27 tons) in more than three years. This momentum and sentiment trade can be witnessed in gold’s cousin, silver, which is up over 50% this year. Precious metals may be going up because they have gone up.

Gold and silver may continue to rally, but the knife cuts both ways for these markets. The last two major bull rallies in gold were followed by bear markets that lasted half a decade, with prices falling by over half. Long-term allocators to gold have needed to be rather patient to earn attractive compound price returns.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.