Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 1.6% for the week.

- Should the Fed be successful in influencing interest rates lower, the resulting benefits for the economy may not be as strong as expected.

Markets expect the Federal Open Market Committee (“FOMC”), the team at the Federal Reserve deciding monetary policy, to lower its overnight target interest rate at its meeting next week. The Fed believes its current effective rate (4.3%) is restrictive for the economy, and a restrictive policy rate does not make sense when employment appears to be cooling down. And, although various measures of inflation remain at levels above the Fed’s 2% target, it does not show signs of strong reacceleration.

It is not given that long-term interest rates, such as those going out 20 or 30 years, will fall should the Fed cut its overnight target rate. The FOMC does not directly control long-term rates, which ultimately determine the cost of mortgages and car loans. The Fed relies on its overnight rate and forward guidance to influence those rates.

Should the Fed ultimately be successful in lowering interest rates along the yield curve, the mainstream view is private sector borrowing and spending would pick up, stoking the economy. Households will be enticed to take out mortgages and refinance their homes at lower rates.

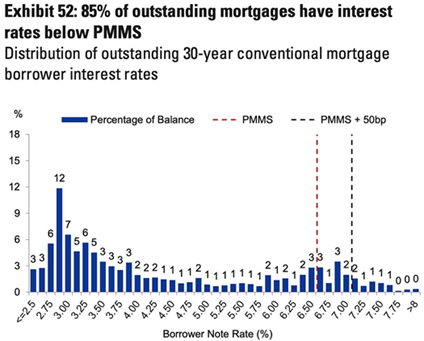

There are a few challenges to this perspective. First, almost all 30-year mortgages have borrowing rates that are below the prevailing 30-year mortgage rate of 6.5% (the “PMMS” dotted line in the chart below). Half of all outstanding 30-year mortgage balances are below 4%. Most existing borrowers are locked into those low rates. It would take a seismic shift down in long-term rates for those mortgages to unfreeze.

Sources: Sam Ro, Goldman Sachs Investment Research, September 2025

Another less-discussed cross-current to the Fed’s rate cutting is that interest income paid to households on their investments would be curtailed. David Kelly at JP Morgan Asset Management notes that American households have $14.0 trillion held in time deposits, money market funds, and short-term investments. Assuming that all of these were fully impacted by Fed rate cuts, he projects that a decline of 1% in short-term interest rates would reduce annual household income by roughly $140 billion. The negative wealth effect would result in less household spending.

Given its evaluative framework and its mandates from Congress, the FOMC is well-justified by employment data if it decides to lower rates next week by 0.25% or even by 0.50%. The Fed would be on course for a “neutral” rather than “restrictive” policy rate. This news may be cheered as stimulative for the economy, but the net benefits of lower interest rates may not be as strong as they appear at first glance.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.