Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, was flat for the week.

- Small-cap stocks performed well in August but have widely underperformed large-caps for several years. Will the factors providing momentum for small-caps persist?

Over the last several years, big stocks in the US market have been outperforming mid- and small-cap stocks, and it has not been particularly close. One oft-cited reason for small-cap misery is the recent rise in interest rates. When the Federal Reserve raised its target interest rate in 2022 to fight inflation, the corporate borrowers most negatively impacted were small companies. They tend to use floating rate debt more than large companies, so as rates moved up, their borrowing rates reset higher.

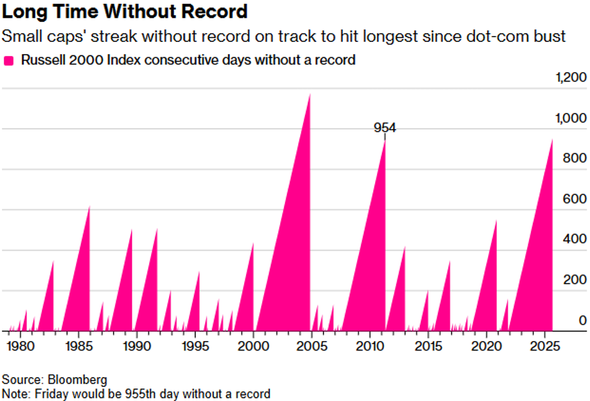

How has recent small-cap suffering compared to history? Bloomberg noted this week that the Russell 2000 index of small-cap stocks has not reached an all-time high for the last two and a half years. That is a long time, comparable only to stretches post-dot-com bubble and post-Great Financial Crisis eras. By contrast, large-caps have notched 19 all-time highs this year alone.

Relevant to the financial health of small companies, lower interest rates may be on the way. In a speech last week in Jackson Hole, Jerome Powell, the chairman of the Federal Reserve, opened the door for rate cuts at the Fed’s next monetary policy meeting in September. The Fed’s view of the balance of risks between inflation and employment is shifting. The Trump Administration is also applying unique pressure upon the Fed in its own quest for lower interest rates.

As expectations for lower interest rates appear to be taking hold, the tiny corner of the stock market where small caps reside has perked up in August. The Russell 2000 is up over 7% this month.

Lower interest rates are helpful, but earnings growth is paramount – and mega-cap technology names have been the companies growing earnings fastest. An environment where the largest companies in the world are growing faster than small companies is peculiar. There is not much precedent.

The tech sector represents only 14% of the benchmark small-cap index, the Russell 2000. It represents about 40% of the Russell 1000 index of large-cap stocks – and perhaps more than that depending on how sectors are sliced and diced. Diversification around the ballooning large-cap US tech sector is prudent. To that end, thoughtful portfolio allocations to small-caps should provide a source of equity returns that is not so beholden to the drivers of returns for mega-cap tech.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.