Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 1% for the week.

- Capital investment in AI infrastructure has propelled the technology sector to all-time high levels relative to the overall US stock market.

In March and early April, the US stock market experienced a peak-to-trough pullback of 19% driven by investor fears over the Trump Administration’s trade policies. That pullback occurred over a 47-day timeframe, a very quick and steep decline.

As it became apparent that the harshest proposed tariffs were not going to materialize, the market snapped back and recovered those losses over the subsequent 79 days, one of the fastest recoveries from a 15%+ pullback in market history. The US market is up close to 10% this year.

Given the prevalence of tariffs and stock market volatility in the news back in the spring, the recovery and subsequent US market strength has been interpreted as the market’s stamp of approval for the current path of trade policy.

Focusing upon tariffs is a misreading of what has driven markets upward this year. The rebound has been driven by the usual suspects: the technology sector and mega-cap tech names. Hyperscalers (large-scale computing providers led by Microsoft, Alphabet, Meta, and Amazon) are investing vast amounts of capital on AI infrastructure. This capital deployment has been compared to the investment in railroads around the turn of the 19th century. By the end of 2026, JP Morgan projects that the hyperscalers will spend over half of their operating cash flow on AI technology. Some estimates have total spending on AI reaching $1 trillion by the end of next year.

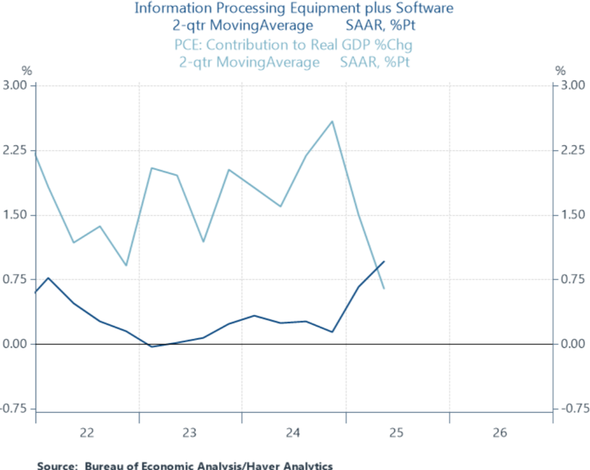

Consumption and consumer spending are the long-term drivers of growth for the US economy. Stunningly, capital investment in AI has contributed more to GDP growth than consumer spending so far in 2025:

Source: Renaissance Macro Research, July 30, 2025

This investment is driving earnings growth in the tech sector, and tech stock prices are soaring as a result. Relative to the S&P 500 index, the tech sector is at all-time highs:

Source: Kevin Gordon, Charles Schwab & Co., 8/5/25

The spending on AI is showing no signs of abating. However, no one can predict where AI is heading, if or when the AI capital spend will slow, or what the hyperscalers are even doing with all this capital formation. Portfolio allocations to other (boring) sectors of the global stock market and to other major asset classes such as (boring) bonds remain important tools for achieving some measure of diversification around the US mega-cap tech-dominated world in which we currently exist.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.