Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, fell 2.6% for the week.

- The 30-year US Treasury bond yield rose above 5% this week. The narratives explaining its rise are a bit unsatisfying.

The 30-year Treasury bond yield rose above 5% this week, its highest level since 2023. The rising 30-year yield occurred in the context of two noteworthy events: the “downgrade” of US Treasury bonds to one notch below AAA by the credit rating agency Moody’s, and the passage of the federal budget bill by the House of Representatives.

Whether the Moody’s downgrade carries a different significance versus the prior downgrades of the US by the two other major ratings agencies, Fitch in 2023 and Standard & Poor’s in 2011, is an open question. Those downgrades did not have a noticeable medium-term impact on markets. Technically, there is no credit or repayment risk facing US Treasury bonds; that risk revolves solely around the politics of the debt ceiling. Once the ceiling is lifted by Congress, the risk vanishes.

The budget passed by the House also received attention in the context of rising long-term yields. A few voices posited that the House budget would widen the federal deficit, increasing expected future bond supply, pushing up long-term interest rates.

The “supply” explanation is unsatisfying for a few reasons. Assuming the baseline is that the prior tax law (the Tax Cuts and Jobs Act of 2017) does not expire, along with countless other assumptions that go into the projection of the federal budget, the bill passed by the House looks to increase the deficit by $180 billion per year over the next 10 years. If that came to fruition, it would not be much incremental issuance for the $30+ trillion US economy and would be absorbed by markets.

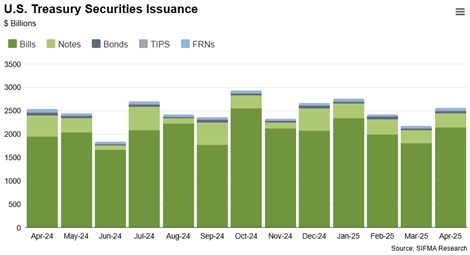

Also, long-term bonds represent a low share of ongoing US Treasury debt issuance and outstanding Treasuries. Most securities issued by the US Treasury are classified as “bills”, which mature in a year or less. “Notes” mature in two, five, seven, and ten years, and “Bonds” mature in 20 and 30 years. “Bonds” are a mere sliver of Treasury debt issuance relative to “bills”:

This is by design. The US Treasury, led by Secretary Scott Bessent, does not issue securities willy-nilly. It is a careful planning process, involving the Treasury Borrowing Advisory Committee (TBAC). The TBAC is a group of “senior representatives from a variety of buy and sell side institutions, such as banks, broker-dealers, asset managers, hedge funds, and insurance companies,” offering guidance on how much debt the Treasury should issue at different maturities.[1]

Long-term bond yields are not only rising in the US. They are also moving higher in Germany and Japan. It could be that it is not supply or Moody’s to blame but simply that the risk of owning long-term bonds is rising, for now.

[1] Luke Kawa, Sherwood News, https://sherwood.news/markets/trumps-top-economic-advisers-debt-issuance-strategy/, February 5, 2025

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2025.