Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, was off 3% for the week.

- The current yield on the US investment grade bond market augurs well for future fixed income returns.

The US investment grade bond market’s average annual return over the last five years through the end of March is distinctly unimpressive. The Bloomberg US Aggregate index, a proxy for the investment grade bond market, returned about 0.5% to investors over that time.

Low returns for bonds are mainly attributable to the low interest rate environment, an environment that goes back longer than five years. In response to lagging growth and non-existent inflation, the Federal Reserve attempted to stimulate the economy with low interest rates. Bond yields fell, which meant that bond prices rose. That felt good to bond investors: rising bond prices are part of the total return.

However, good contemporaneous returns on bonds due to falling yields and rising bond prices masked the underlying bond math: returns going forward would almost certainly be lower as a result. The unfolding low-rate environment meant that as bonds matured and interest payments were received, bond investors faced growing reinvestment risk – the risk of investing cash flows at lower interest rates.

Fixed income investors were slammed in 2022 when the Federal Reserve jacked interest rates up to stifle inflation, which made a flamboyant post-COVID reappearance around the world. Yields shot up. Bond prices fell.

This recent experience has led investors to question allocations to bonds at all. What is the point of an asset class that has delivered such low returns?

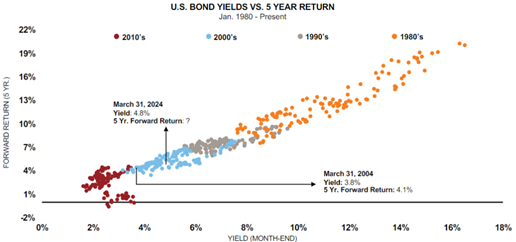

The first answer to this question may be found in the chart below from Russell Investments. It shows historical yields of the Aggregate bond index (the x-axis) and the five-year forward total returns for those yields (the y-axis). There is a tight relationship between the two: the best predictor of future returns for bonds is their current yield. The current bond market yield is 4.8%, which is consistent with forward five-year bond returns of between 4 and 6% per year.

Source: Russell Investments, March 31, 2024

The other reason for allocations to bonds is they are meant to act as the “shock absorber” in portfolios to cushion against inevitable volatility in stocks. Over the last two years, rising bond yields have been a source of stock market volatility, leading some to claim that bonds no longer serve such a role in portfolios. However, short- and intermediate-duration bonds remain far less volatile than stocks. Allocations to fixed income will lower overall portfolio volatility.

Long-term investors who can ride through extended stretches of equity volatility may rightly question allocations to fixed income in portfolios. Stocks are expected to outperform bonds over the long haul. For investors with shorter time horizons or those who seek a lower portfolio risk profile, bonds will continue to serve that purpose.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication.

Copyright Indiana Trust Wealth Management 2024.